In the fast-evolving world of fintech and digital payments, Asima, developed by Kieron James and the team behind Wonderful, is bringing a refreshingly grounded, ethical, and transparent approach to open banking infrastructure. While most players in this space race toward complexity and scale, Asima is proving that simplicity, trust, and customer alignment are just as powerful.

What Asima Does and Who It’s For

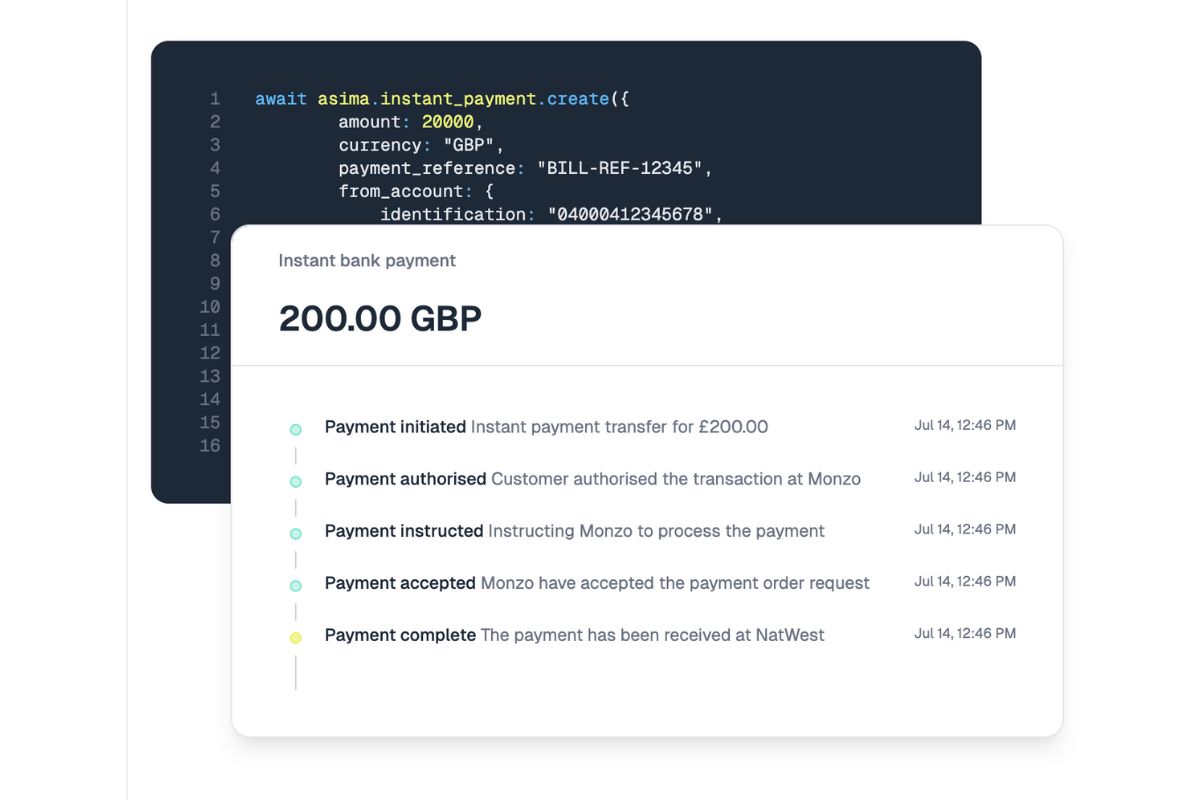

Asima powers UK high-growth operations with open banking services. It offers “regulated rails for account access and instant bank payments,” built specifically for enterprises seeking more control and efficiency in how they manage their finances. From fintechs and lenders to charities and wealth management platforms, Asima provides the infrastructure for instant, secure account-to-account transactions and smart data flows.

Its ideal customers are CTOs, product leads, and innovation teams in mid-to-large-sized businesses who are ready to embed open banking deeply into their platforms, but need the stability, support, and regulatory trust to make that leap.

How the Idea Was Born

Asima didn’t start as a product roadmap; it began as a mission. The team first built open banking infrastructure for Wonderful, a platform enabling fee-free donations for UK charities. What began as a “genuine tech-for-good mission and a completely philanthropic project” soon became something much larger.

As open banking adoption grew, Wonderful began extending its secure and cost-effective payment rails to small businesses. That organic expansion opened the floodgates.

“We extended the same cost-saving, secure payment rails to small businesses. That expansion led to a surge in inbound enquiries from enterprise teams... asking if they could leverage our infrastructure.” The result was Asima, created to meet the demand for enterprise-grade infrastructure, already “battle-tested in the real world.”

The Challenges and How They Were Overcome

Asima’s journey hasn’t been challenge-free, but its approach to tackling those hurdles reflects the company's core values of trust and transparency. The biggest challenge right now? Focus.

“We see opportunity almost everywhere we look, which is an exciting position to be in. As a small, fast-growing team, our biggest challenge is prioritising the projects that will deliver the most value to our customers.”

With so much demand coming from multiple industries, each with unique use cases, maintaining a clear and strategic roadmap becomes critical. The team is careful not to spread itself too thin, even if the temptation is strong. That focus allows Asima to keep quality and service high, especially in a landscape where every product decision impacts compliance, customer trust, and long-term scale.

Another lesson came early and came hard.

“One key lesson we’ve learned is that great tech isn’t enough on its own. You have to meet customers where they are.”

In the early days, the team assumed that open banking's ethical and cost-saving appeal would be enough to win over customers. But adoption wasn’t automatic. “The reality is, timing, trust, and ease matter just as much.” That realization led to a renewed focus on onboarding, clearer messaging, and simplifying the experience so that switching to open banking didn’t feel risky; it felt inevitable.

Trust First, Revenue Second

Rather than leaning on aggressive marketing or hidden fees, Asima has built its reputation through consistent transparency. Their roots in the charity sector made honesty and clarity non-negotiable. “What’s consistently driven growth is trust, earned through transparency, not marketing spin.” This meant clear pricing, upfront data usage policies, and strong service guarantees, especially for customers “tired of opaque costs and legacy providers.”

This has led to strong growth, especially when combined with their disruptive pricing model. “Offering disruptive pricing at just 1p per transaction, with no percentage fees via Wonderful, while delivering genuinely robust infrastructure, built confidence fast.”

It’s not just about moving fast or cutting costs—it’s about building the kind of company people want to work with long term.

Built for Scale, Priced for Trust

What sets Asima apart is that it doesn’t just offer the tech; it provides the strategic partnership needed to use that tech well. “Most open banking infrastructure providers focus on either raw API access with limited support, or consumer-facing apps with little flexibility for enterprise integration.”

By contrast, Asima offers mature infrastructure paired with “architecture, compliance, product design, not just endpoints.” For those who want to self-serve, that’s available too. But the real value lies in having the people and the platform needed to make enterprise-scale open banking work, all backed by FCA authorisation and a track record across sectors.

It’s no wonder that Asima now processes more transaction value each month through open banking than they ever did through traditional debit and credit cards, a milestone that speaks volumes about their impact and momentum.

What’s Next and Where to Find Them

With a solid product, growing demand, and strong ethics at its core, Asima is poised to become a major player in the open banking landscape. For a small team, scaling without compromising their values is the next big goal. As the platform evolves, the team is staying focused on the one thing that got them here: listening to what customers really need, and building from there.

If you’re an enterprise exploring open banking, struggling with outdated payment systems, or simply looking for an infrastructure partner you can trust, Asima may be exactly what you need.

To learn more, you can visit Asima or Wonderful, or connect directly with founder Kieron James on LinkedIn.